FieldAI closed the summer of 2025 with a staggering raise: $405 million across consecutive Series A and A1 rounds, the latter a $314 million tranche co-led by Bezos Expeditions, Prysm, and Temasek. The round was oversubscribed, according to the company, and valued the two-year-old startup at roughly $2 billion. Eighteen months after incorporation, FieldAI became a robotics unicorn without ever shipping a robot. The cap table is worth reading carefully, because it tells a specific story about where the smart capital in embodied AI believes the margin will land.

The round structure

The funding came in two tightly sequenced tranches, a Series A and a Series A1, announced together in August 2025. The $314 million Series A1 was co-led by three investors that rarely sit on the same side of a table: Jeff Bezos’s family office, a Middle Eastern growth fund, and Singapore’s sovereign wealth vehicle. Oversubscription typically signals either unsatisfied demand or strategic allocation tension, both healthy signals for a Series A-stage company.

The cap table as thesis document

The investor list is less a syndicate than a thesis statement:

- Bezos Expeditions, Jeff Bezos’s personal vehicle. Already an investor in Skild AI, Physical Intelligence, and Figure. Bezos is making the same bet across at least four competing robot-brain companies, which is itself a statement about how he reads the category.

- Temasek, Singapore’s sovereign fund, a patient-capital signal. Temasek rarely moves into private-company positions at this stage unless it sees a decade-long hold.

- Prysm, growth investor, co-lead of the latest round. Adds follow-on firepower for the next tranche.

- NVIDIA NVentures, strategic stake in anyone building serious robotics workloads on NVIDIA silicon. Also invested in Skild AI. NVIDIA’s thesis: the silicon wins regardless of which brain wins.

- Intel Capital, enterprise distribution angle, particularly into industrial and energy customers.

- Khosla Ventures, long-standing AI-infrastructure conviction shop. Vinod Khosla has been consistently early on infrastructure plays from Stripe to OpenAI.

- BHP Ventures, the venture arm of one of the world’s largest mining companies. Strategic customer signal: mining is a $3–4 billion autonomous-robotics opportunity by 2030.

- Emerson Collective, Laurene Powell Jobs’s firm, long-horizon, impact-tilted.

- Canaan Partners, earlier-stage holdover, continuing participation.

- Gates Frontier, Bill Gates’s climate-and-frontier-tech vehicle, previously invested.

- Samsung, previous investor, strategic angle on humanoid and consumer robotics.

The absences are also notable. No SoftBank, which went deep on Skild AI with a $1.4 billion Series C lead. No Alphabet, which led Physical Intelligence’s $600 million Series B. The three top robot-brain companies appear to have deliberately non-overlapping strategic lead investors, a pattern that mirrors the early days of the LLM wars, where OpenAI took Microsoft, Anthropic took Google and Amazon, and Cohere split Salesforce and Oracle.

The comparables

The “robot brain” category is now one of the most concentrated capital flows in tech:

| Company | Latest valuation | Latest round | Lead investor | Founded |

|---|---|---|---|---|

| Skild AI | $14B | $1.4B Series C (Jan 2026) | SoftBank | 2023 |

| Physical Intelligence | $5.6B | $600M Series B | Alphabet | 2024 |

| FieldAI | $2B | $314M Series A1 (Aug 2025) | Bezos / Prysm / Temasek | 2023 |

FieldAI is the smallest of the three by valuation, but the one with the clearest field-robotics specialization and the deepest government-grade autonomy pedigree. CEO Ali Agha spent seven years at NASA’s Jet Propulsion Laboratory leading DARPA Subterranean, DARPA RACER, and the Mars Helicopter–Rover coordinated autonomy program. Neither Skild nor Physical Intelligence has comparable field-deployment credentials.

What investors are actually buying

Three distinct bets sit inside the FieldAI thesis:

- The layer hypothesis. Robotics bifurcates into commoditized hardware and high-margin software, and the brain wins the margin. The Android-versus-handset-OEM analogy is the one most investors use in conversation. FieldAI is pure-play on the software side, which makes it a cleaner bet than any vertically integrated humanoid company that has to justify hardware gross margins alongside software.

- The physics-first moat. If VLA approaches hit a reliability ceiling, and there is early evidence they do, especially in safety-critical deployments, then a probabilistic, risk-aware architecture becomes the only path to insurable, certifiable deployments. This is particularly relevant under the EU AI Act and evolving ISO safety standards, which will demand certified autonomy layers. Hard to catch up to without a decade of DARPA and NASA data.

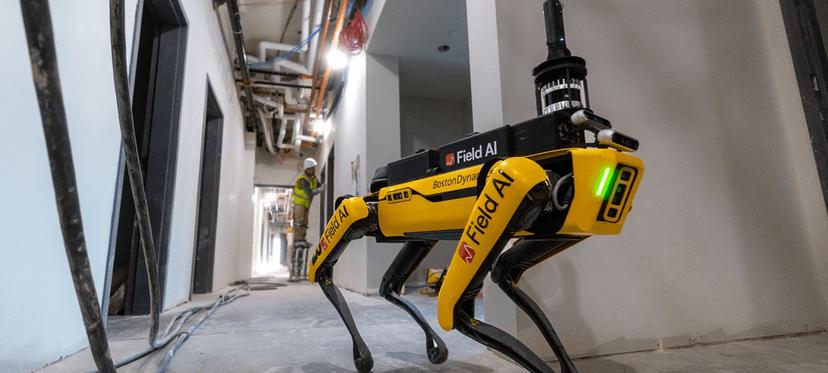

- The distribution flywheel. Every embodiment FieldAI supports, Spot, other quadrupeds, humanoids, wheeled platforms, passenger vehicles, compounds into training data without requiring FieldAI to own hardware margins. The Boston Dynamics partnership announced in March 2026 is the first public proof point that this flywheel is spinning.

The business model behind the valuation

FieldAI runs a B2B hybrid model: sensor-compute payloads paired with edge-based software licensing. Revenue flows from hardware integration fees on installation and recurring software licenses afterward. The hardware-agnostic strategy means existing customer fleets, Boston Dynamics Spots, ANYbotics ANYmals, third-party humanoids, can be retrofitted rather than replaced, which dramatically shortens sales cycles.

Revenue figures are not public, but Sacra notes “rapid customer adoption and multiple expansion contracts” as the justification for the oversubscribed raise. Deployments span construction, energy, manufacturing, urban delivery, and inspection across Japan, Europe, and the United States. Known customers include DPR Construction. The rest are under NDA.

The headcount signal

FieldAI said it has added more than 100 employees in the months leading up to the raise, with plans to double headcount again by the end of 2025. Hiring skews toward locomotion and manipulation R&D, a signal that the next capability frontier is complex dexterous work, not just navigation. Manipulation is where VLA approaches have made the loudest demos; it’s where FieldAI needs to prove its physics-first architecture can scale beyond mobility.

The risk the cap table is underwriting

The same embodiment-agnostic pitch is being made by Skild AI with seven times the capital and by Physical Intelligence with Alphabet’s compute and distribution muscle. If the brain layer converges to one or two winners, the most common outcome in platform markets, being the smallest of the three unicorns is a precarious place to sit.

Three risks are explicit in the category:

- Model generalization at scale is technically unproven. No one has shown that a single foundation model can handle the diversity of real industrial environments without significant per-deployment tuning. The first company to prove it unlocks the platform thesis. The rest compete for niches.

- Hardware dependency may face obsolescence as robots begin to ship with standardized autonomy interfaces. If Spot, Atlas, and ANYmal all converge on a common API, the brain layer commoditizes.

- OEM competitive displacement. Large manufacturers may develop internal autonomy rather than license from a startup. Boston Dynamics partnering with FieldAI is a strong counter-signal, but Figure, 1X, Agility, and Tesla have all publicly committed to building their own brains.

The next eighteen months

The next eighteen months will decide whether $405 million was a down payment on a category, or a premium for a niche. The checkpoints to watch are straightforward: does the Boston Dynamics partnership convert into expanded deployments? Does FieldAI land a second major hardware platform partner? Do manipulation deployments hit production scale? Does a European energy or Japanese construction major disclose a multi-year rollout?

If the answers skew positive, the $2 billion valuation will look, in retrospect, like the entry price. If they skew mixed, Skild AI and Physical Intelligence will continue pulling ahead on capital, and FieldAI will need to find a specialty, field robotics, safety-certified autonomy, government and defense, where the physics-first approach is irreplaceable.

Either way, the cap table has already rendered its verdict on where the margin is going. The rest is execution.